The OECD's Rosy Glasses: A Closer Look at "Resilience"

The OECD is singing a relatively upbeat tune, revising upwards its growth forecasts for the US and Eurozone. "Surprisingly resilient," they call the global economy. But let's pump the brakes on the parade for a minute. Resilient is a strong word. It suggests an inherent ability to bounce back from adversity. Is that really what we're seeing, or are we just witnessing the effects of some clever (or desperate) macroeconomic Band-Aids?

Unpacking the Drivers of "Resilience"

The report highlights easier global financial conditions, supportive macroeconomic policies, real income growth, and strong AI-related investments as the drivers. Okay, let's unpack that. "Easier financial conditions" often means lower interest rates or increased liquidity – essentially, kicking the can down the road. "Supportive macroeconomic policies" can range from targeted fiscal stimulus to simply printing more money. And "real income growth"? Well, that depends heavily on how you slice the inflation data. (Remember that inflation, even if slowing, is still cumulative.)

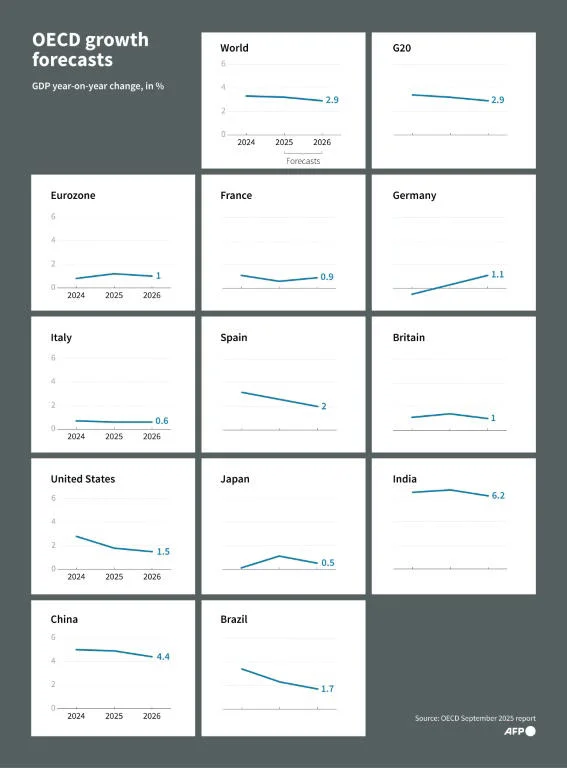

The OECD projects US GDP growth at 2.0% in 2025, a 0.2-point bump from their previous forecast. The Eurozone is expected to hit 1.3%, up 0.1 points. China is pegged at 5.0%. These are incremental adjustments, not seismic shifts. The global economy is expected to grow 3.2% in 2025, down from 3.3% in 2024, before slowing to 2.9% next year, and rebounding again in 2027, when a 3.1-percent expansion is forecast. The question, of course, is how they arrive at these projections. What assumptions are baked into the model?

The Devil in the Details: Methodology and Assumptions

I've looked at hundreds of these economic outlooks, and the devil is always in the details of the methodology. Are they properly accounting for the lagged effects of tighter monetary policy? Are they accurately forecasting consumer behavior in the face of persistent inflation? And what about the geopolitical wildcards – the potential for escalating conflicts, trade wars, or unexpected supply chain disruptions? The OECD acknowledges these "downside risks," but how are they factored into the baseline scenario?

AI: Savior or Bubble?

The elephant in the room, of course, is AI. The OECD specifically calls out "strong demand for new AI-related investments, particularly in the US" as a supporting factor. This is where my skepticism really kicks in. We're seeing a surge in valuations for AI-related companies, driven by hype and speculation, not necessarily by concrete earnings. The OECD itself warns about "high asset valuations based on optimistic expectations of AI-driven corporate earnings." It's a classic bubble scenario.

Think of it like the dot-com boom of the late 90s. Back then, any company with ".com" in its name saw its stock price skyrocket, regardless of its actual business model or profitability. Are we making the same mistake with AI? Are we overestimating its near-term impact and underestimating the risks? The OECD is right to flag the potential for "abrupt price corrections." But how severe could those corrections be? And what would be the knock-on effects for the broader economy?

Inflation and the Tightrope Walk

Eurozone inflation, meanwhile, inched up to 2.2% in November. Eurozone inflation inches up to 2.2 pct in November The ECB left its key rate unchanged for the third consecutive time in October, after inflation fell from more than 10 percent in 2022 to settle around the bank's two-percent target. This is the tightrope walk central banks are attempting: keeping inflation in check without triggering a recession.

The "Resilience" Narrative: Premature?

The OECD's assessment feels…premature. Yes, the global economy hasn't completely collapsed, but that doesn't mean it's inherently resilient. It means we've been throwing a lot of resources at keeping it afloat. The question is, can we sustain that level of intervention indefinitely? And what happens when the stimulus fades, the interest rates rise, and the AI bubble bursts? The real test of resilience is yet to come.

Is This Just the Eye of the Storm?

The OECD paints a picture of "surprising resilience," but I see a system propped up by artificial supports and vulnerable to shocks. The AI boom could be a genuine engine of growth, or it could be the biggest misallocation of capital since…well, since the last tech bubble. Until we see more concrete evidence of sustainable, broad-based growth, I'm not buying the "resilience" narrative.

")